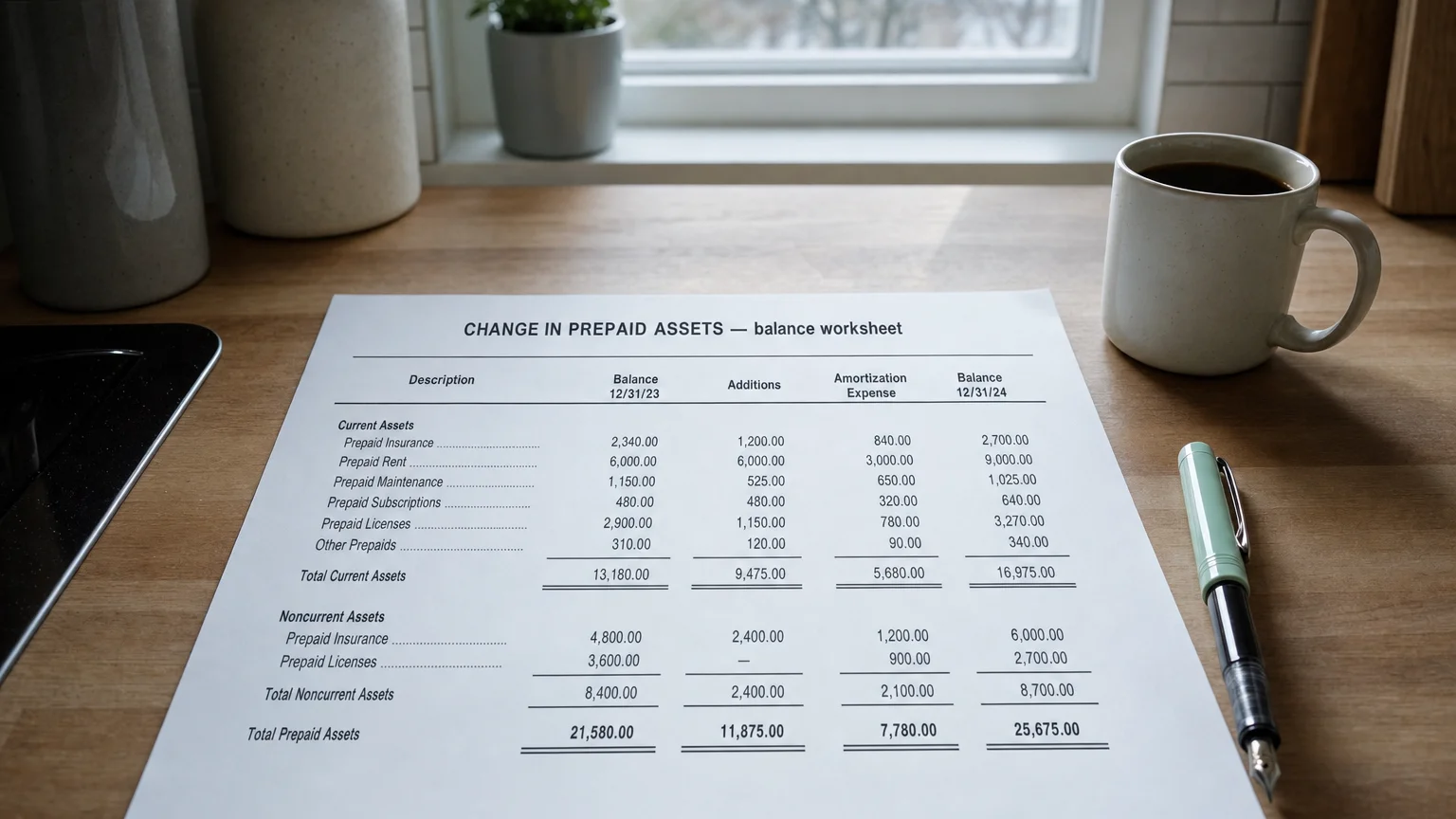

Change in prepaid assets is the net increase or decrease in advance payments for future benefits during the period. An increase subtracts from operating cash flow because cash was paid before the expense is recognized; a decrease adds back as prior prepayments are expensed.

If you aren't willing to own a stock for ten years, don't even think about owning it for ten minutes.

Change in Prepaid Assets is the net increase or decrease in prepaid expenses (advance payments for goods/services) during the reporting period. This line appears in the operating activities section of the indirect-method cash flow statement. An increase subtracts from operating cash flow (cash paid upfront exceeds expense recognized), while a decrease adds back (prior prepaids now expensed without new cash out).

What It Really Means

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1996 (1996)

Prepaid assets are cash you’ve already spent for future benefits—like insurance or rent paid ahead.

When prepaids grow, you’ve paid more cash than the expense hitting the income statement—cash leaves faster than profit reflects, reducing operating cash flow. When they shrink, you’re expensing old prepaids without new cash out—boosting OCF.

A Clear Example

Company switches to annual insurance prepayment for discount.

- Prior year: Monthly payments → minimal prepaid

- This year: Pay $120k for full year coverage upfront

- Prepaid Assets rise by $100k (after monthly amortization)

- Cash flow this year: -$100k Change in Prepaid Assets (subtract)

- Next year: No new big payment → prepaids fall as expensed → + cash flow

This year cash feels the hit; next year gets the benefit.

Common Drivers

- Shift to annual prepayments (insurance, software licenses)

- New long-term contracts or leases

- Bulk purchases for discounts

- Timing of rent or advertising payments

- Growth requiring more advance commitments

Fast-growing or seasonal businesses often show increases.

How It Fits in Cash Flow

Indirect method operating section:

- Net Income (includes portion of prepaid expense)

- − Increase in Prepaid Assets (or + Decrease)

- = Cash from Operations

It’s a working capital adjustment for prepayment timing.

What a Change Tells You

- Rising → cash tied up in advance payments (OCF drag)

- Falling → freeing prior cash commitments (OCF boost)

- Link to growth (more prepaids for expansion)

- Efficiency (bulk prepay discounts?)

- Future expense relief (next period lower cash needs)

Compare to revenue growth—prepaids rising faster may signal scaling commitments.

Q · 01Why does rising prepaid assets reduce operating cash flow?+

Q · 02How do shrinking prepaids improve operating cash flow?+