Change in inventory is the period-over-period difference in a company’s stock balance. An inventory increase is a cash outflow; a decrease is a cash inflow. Both appear in Operating Activities as working capital adjustments to net income.

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

Change in Inventory refers to the period-over-period difference in a company’s inventory balance—that is, how much the value of its goods and products held for sale increased or decreased. Inventory is a current asset, and its change is a key component of working capital adjustments on the cash flow statement. This figure shows how much cash a company has tied up in its stock.

The Link Between Inventory and Cash Flow

“No asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Changes in inventory are a crucial adjustment in the Operating Activities section of the cash flow statement. This is because buying more inventory ties up cash, while selling down inventory frees up cash. The income statement reports the Cost of Goods Sold on an accrual basis, but it doesn’t show the cash spent to build up or maintain stock levels. The cash flow statement adjusts for this timing difference. If a company spends cash to produce or purchase more goods than it sold, that cash has been used, and this must be reflected to get a true picture of operational cash flow.

Increase vs. Decrease: A Use or Source of Cash?

The Core Rule

How It’s Calculated and Presented

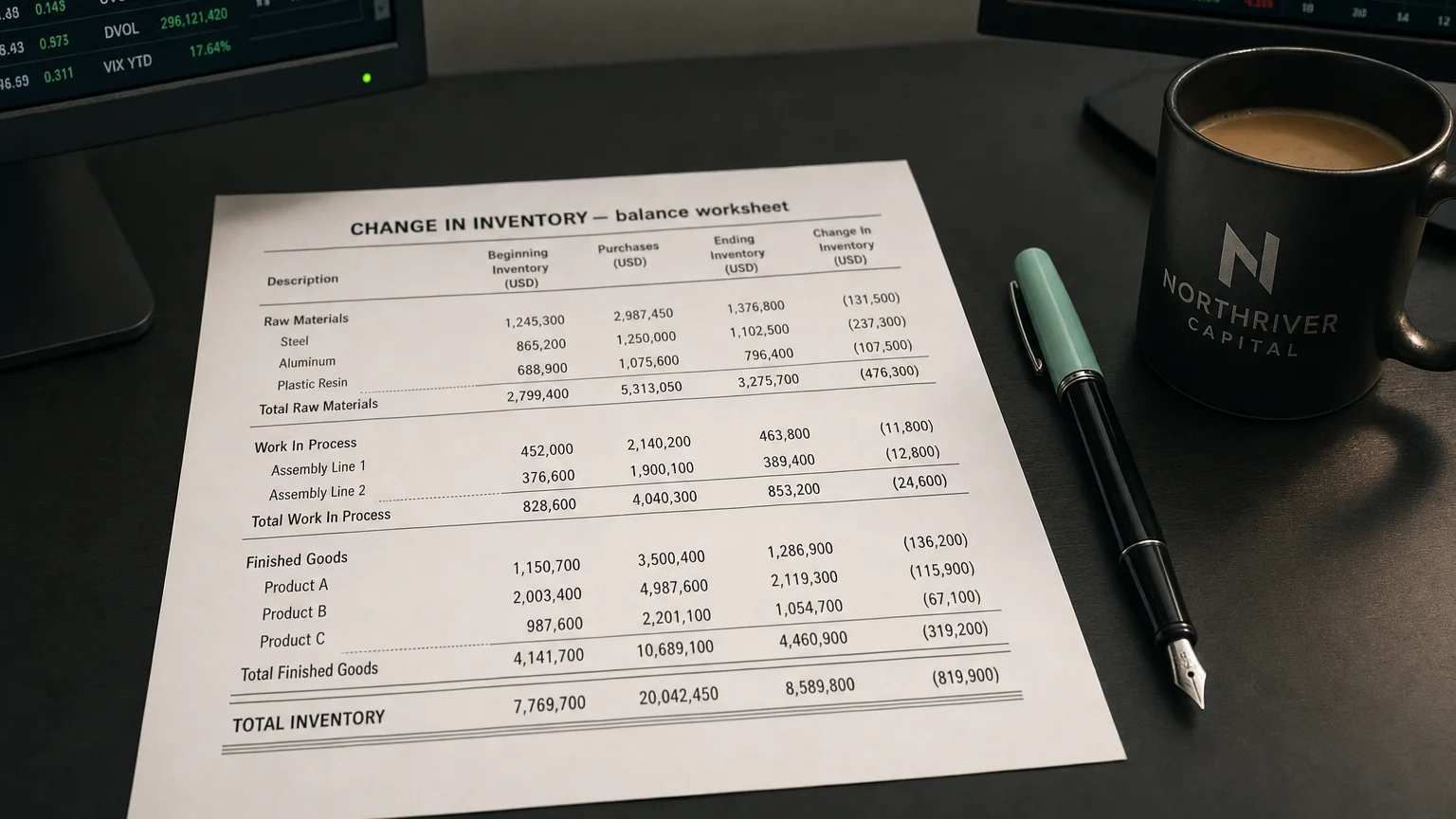

The change in inventory is calculated by comparing the inventory balances from the balance sheet at two different points in time.

Formula:

For the cash flow statement, the sign of the cash impact is the opposite of the change. If inventory increases by 10,000 change), this is shown as a -10,000 (a -10,000 adjustment (a cash inflow). This line item appears in the Operating Activities section, often labeled as ‘(Increase) Decrease in Inventory’.

What Inventory Movements Reveal About a Business

Analyzing inventory changes provides significant insight into a company’s operational efficiency and market position. A large increase in inventory might signal several things:

- Anticipation of Growth: The company may be stocking up in preparation for higher future sales.

- Slowing Demand: Alternatively, it could be a red flag that products are not selling as quickly as expected, leading to a stockpile of unsold goods.

- Reduced Liquidity: In either case, growing inventory ties up cash that could be used for other purposes, which can strain liquidity.

On the other hand, a decrease in inventory often indicates:

- Strong Sales: The company is selling goods faster than it is replacing them.

- Improved Efficiency: The business may be effectively managing its stock levels (e.g., through just-in-time systems), freeing up cash and improving operating cash flow.

- Risk of Stockouts: If inventory falls too low, it could signal a risk of being unable to meet customer demand.

Investors watch these changes closely, as they affect cash flow and can reveal strengths or weaknesses in a company’s day-to-day financial management.

Example in a Cash Flow Statement

Simplified Cash Flow Statement (Indirect Method)

Cash Flows from Operating Activities

Net Income: 10,000 **Change in Inventory: -15,000 Change in Accounts Payable: +$15,000

In this scenario, the **-30,000 during the period. This increase was a $30,000 use of cash, so it is subtracted from net income.

Q · 01How does rising inventory affect the cash flow statement?+

Q · 02What signals does a falling inventory balance send to analysts?+

Q · 03What is the formula for calculating change in inventory?+