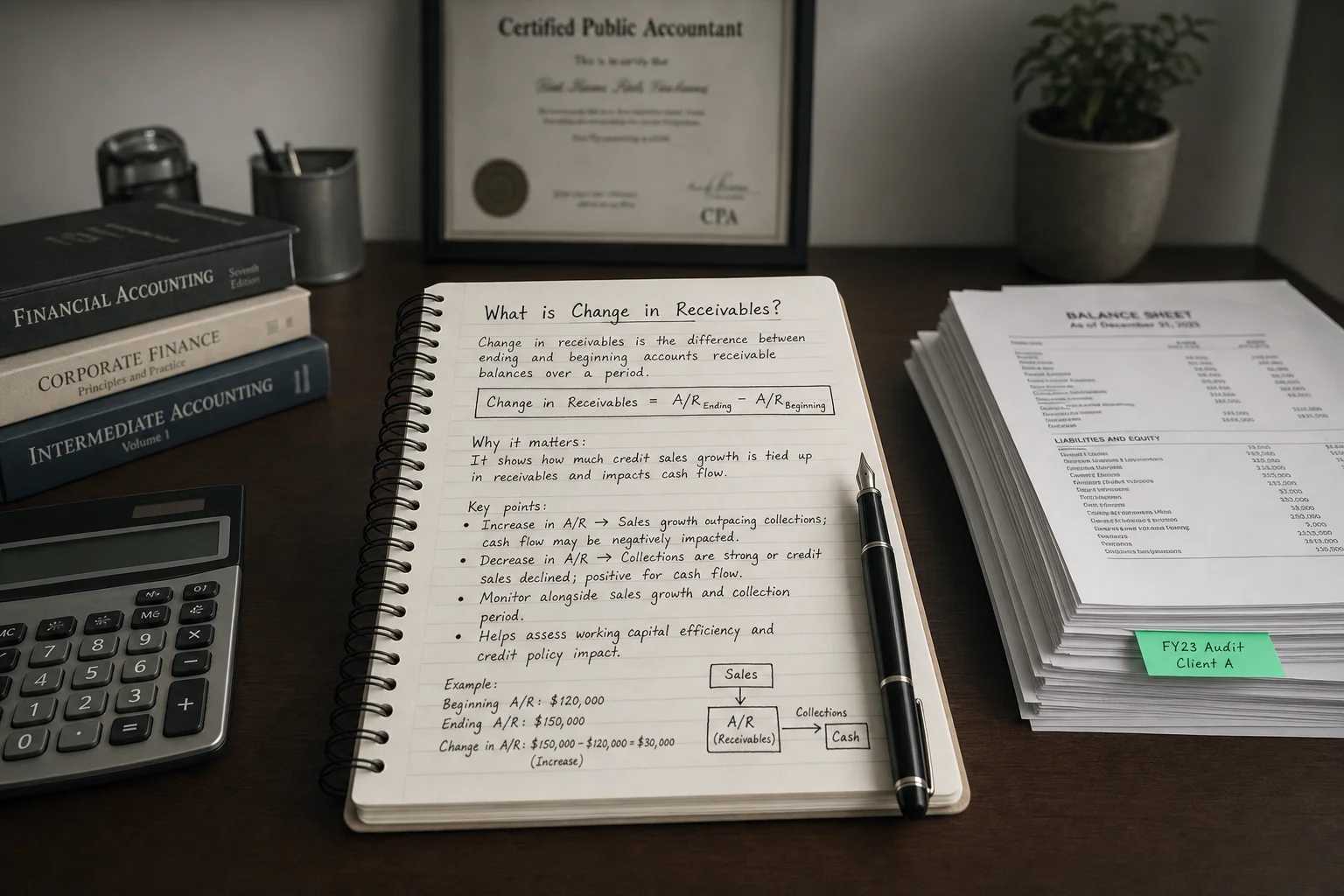

Change in receivables is the period-over-period difference in accounts receivable on the cash flow statement. An increase subtracts from operating cash flow — revenue was booked but cash not yet collected; a decrease adds back as prior balances are converted to cash.

The intelligent investor is a realist who sells to optimists and buys from pessimists.

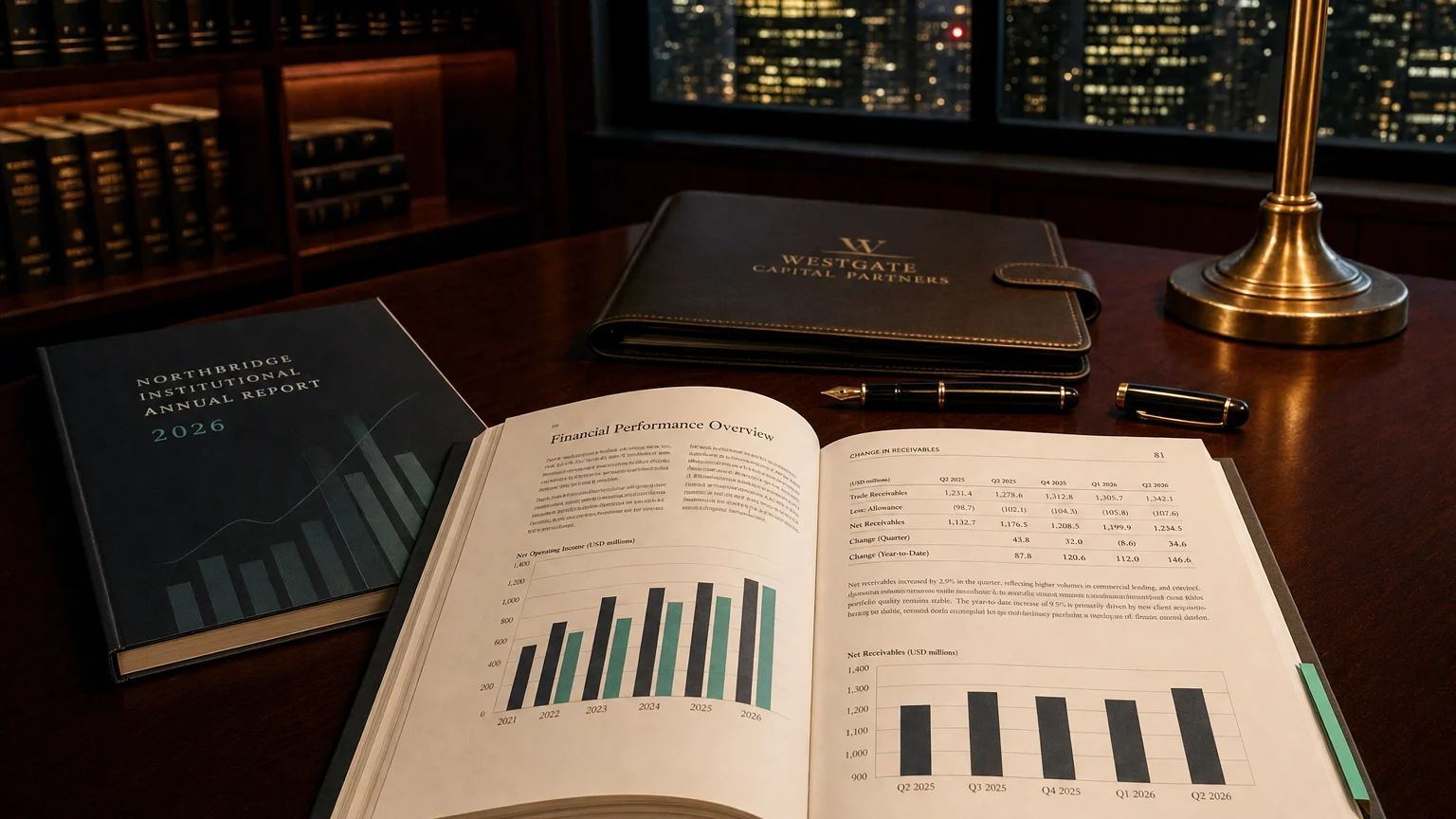

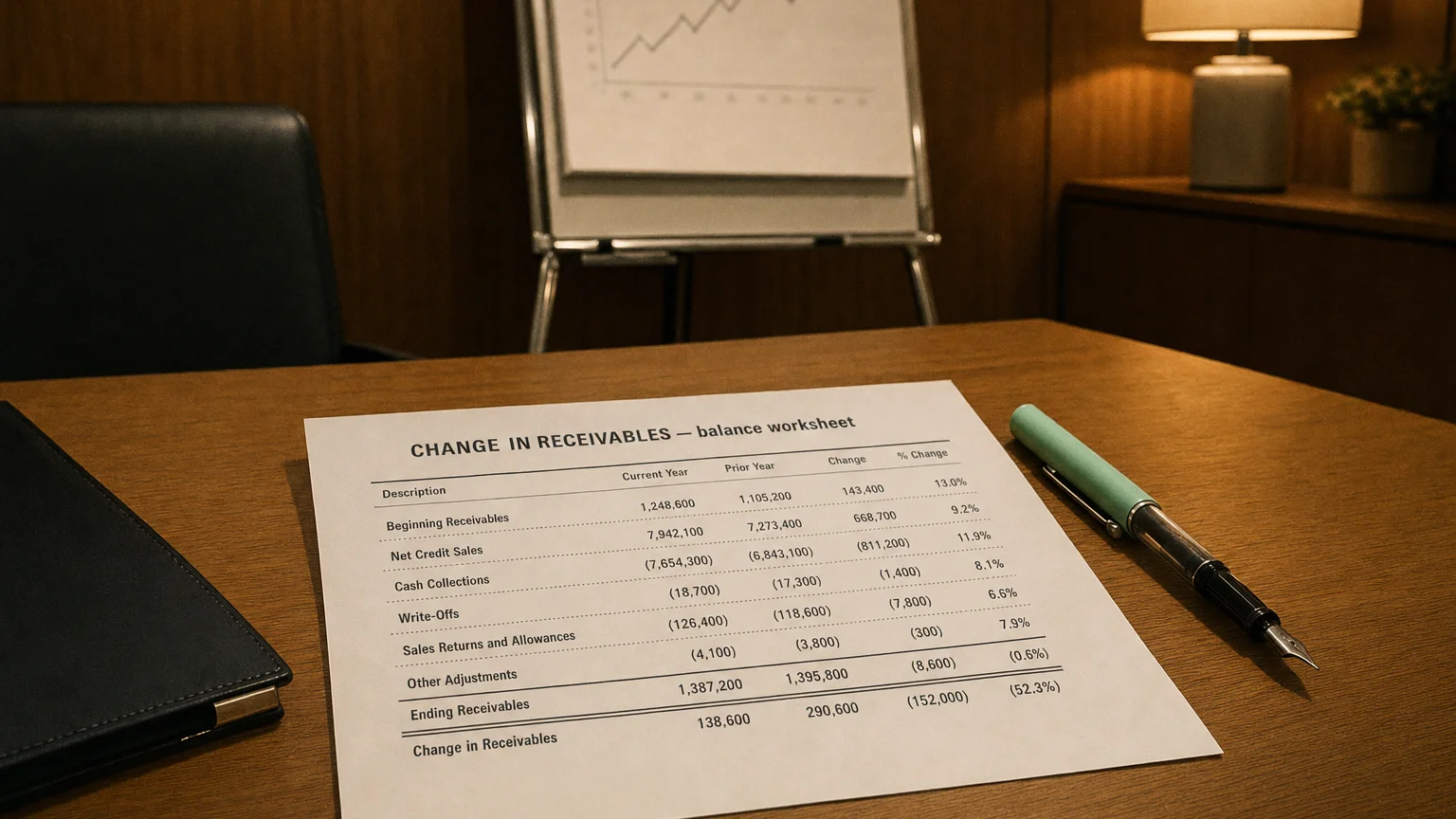

On a cash flow statement, change in receivables refers to the period-over-period difference in a company’s accounts receivable (AR). Accounts receivable are amounts owed by customers for sales made on credit—effectively, money the company has earned but not yet received in cash. This line item shows how much the AR balance has increased or decreased, providing a crucial adjustment for reconciling net income to actual cash flow by highlighting the conversion (or lack thereof) of sales into cash.

The Link Between Sales, Receivables, and Cash

“The intelligent investor is a realist who sells to optimists and buys from pessimists.”

— Benjamin Graham, Author, The Intelligent Investor The Intelligent Investor (1949)

Changes in receivables impact operating cash flow because of the timing difference between when revenue is recorded and when cash is collected. Under accrual accounting, a credit sale boosts revenue and net income immediately, even though no cash has changed hands. If accounts receivable increases, it means the company recorded more in sales than it collected in cash from customers. This reduces the actual cash flow relative to the reported net income. Conversely, if receivables decrease, it means cash collections from past sales exceeded new credit sales, boosting cash on hand. This adjustment is essential for showing the true cash impact of sales activities.

Increase vs. Decrease: A Use or Source of Cash?

The Core Rule (Inverse Relationship)

How It’s Calculated and Presented

The change is calculated by comparing the accounts receivable balance at the beginning of a period to the balance at the end. It appears in the Operating Activities section of the cash flow statement (indirect method).

Formula:

For example, if AR was 120,000 this year, the balance increased by 20,000** adjustment (a use of cash). This line is often labeled as ‘(Increase)/Decrease in Accounts Receivable’.

Significance for Business Analysis

This line item is a vital indicator of a company’s financial health, collection efficiency, and quality of earnings.

- Insight into Collections and Credit Policy: A large increase in receivables may suggest the company is struggling to collect from customers or has loosened its credit terms, tying up cash. A decrease suggests strong collections or tighter credit policies.

- Liquidity and Working Capital Impact: Rising receivables can strain a company’s liquidity, as profit is ‘locked’ in unpaid invoices. A company can be profitable on paper but unable to pay its bills if it can’t convert receivables into cash.

- Quality of Earnings: If net income is growing but AR is growing even faster, it could be a red flag. It may indicate that the company is aggressively booking credit sales that are not translating into cash, a sign of low-quality earnings.

- Working Capital Management Efficiency: Analysts use metrics like Days Sales Outstanding (DSO) to assess how quickly a company collects its receivables. A stable or declining DSO, reflected in manageable changes in receivables, suggests efficient working capital management.

Example in a Cash Flow Statement

Simplified Cash Flow Statement (Indirect Method)

Cash Flows from Operating Activities

Net Income: 10,000 Increase in Accounts Receivable: -5,000 Increase in Accounts Payable: +108,000

Here, the **-15,000. This is treated as a use of cash, as $15,000 of reported revenue has not yet been collected.

Q · 01Why does growing accounts receivable reduce operating cash flow?+

Q · 02What does a shrinking receivables balance tell investors?+