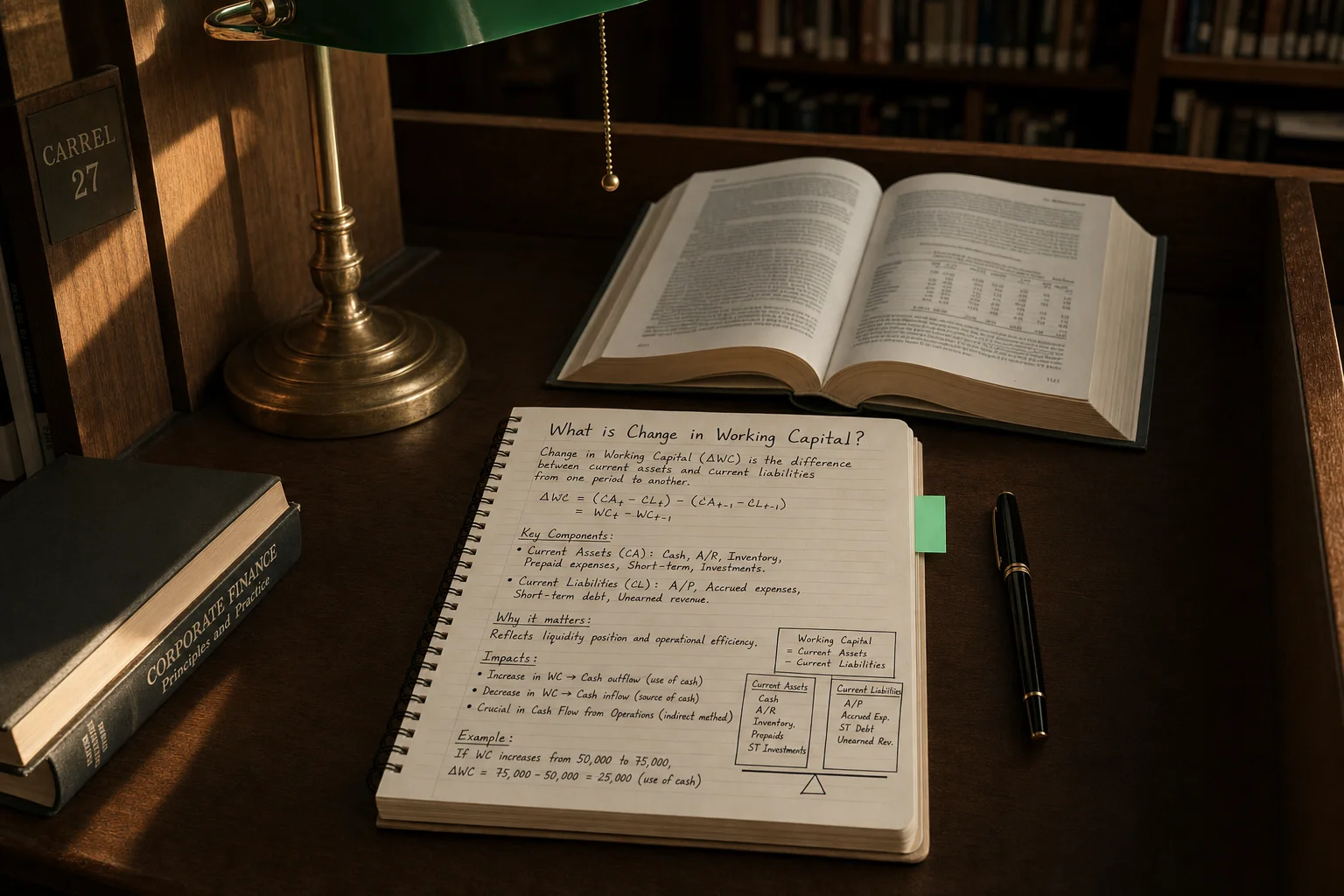

Change in working capital is the net shift in current assets and liabilities between periods. Rising current assets consume cash; rising current liabilities conserve it. These adjustments reconcile accrual-based net income to actual operating cash flow.

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

Working capital is the difference between a company’s current assets and current liabilities. Current assets include items like cash, inventory, and accounts receivable (money owed by customers), while current liabilities include accounts payable (bills owed), short-term debt, and other obligations due within a year. A positive working capital (assets > liabilities) suggests the company can meet its short-term obligations. In financial analysis, the change in working capital between periods is a critical adjustment used to understand a company’s true cash flow from operations.

Why Changes in Working Capital Affect Cash Flow

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (Graham & Dodd, 1st edition 1934); restated in The Intelligent Investor (4th rev. ed., 1973), Chapter 1, p. 18 (1934)

Working capital ties up cash in daily operations, so its changes directly impact cash flow. Increasing current assets (like buying more inventory or letting customers buy on credit) uses cash (a cash outflow), whereas increasing current liabilities (like delaying payments to suppliers) preserves cash (a cash inflow). A cash flow statement’s purpose is to reconcile accrual-based net income to actual cash, which requires adjusting for these non-cash changes.

For example, if a company’s sales grow on credit, accounts receivable increase, but the cash hasn’t yet been collected. The cash flow statement must subtract that increase from net income. Conversely, if a firm delays paying its suppliers, its accounts payable increase, which means it held onto its cash longer. The cash flow statement adds back that increase. These adjustments ensure the statement shows the true cash generated or used by the business.

How It Is Calculated and Presented

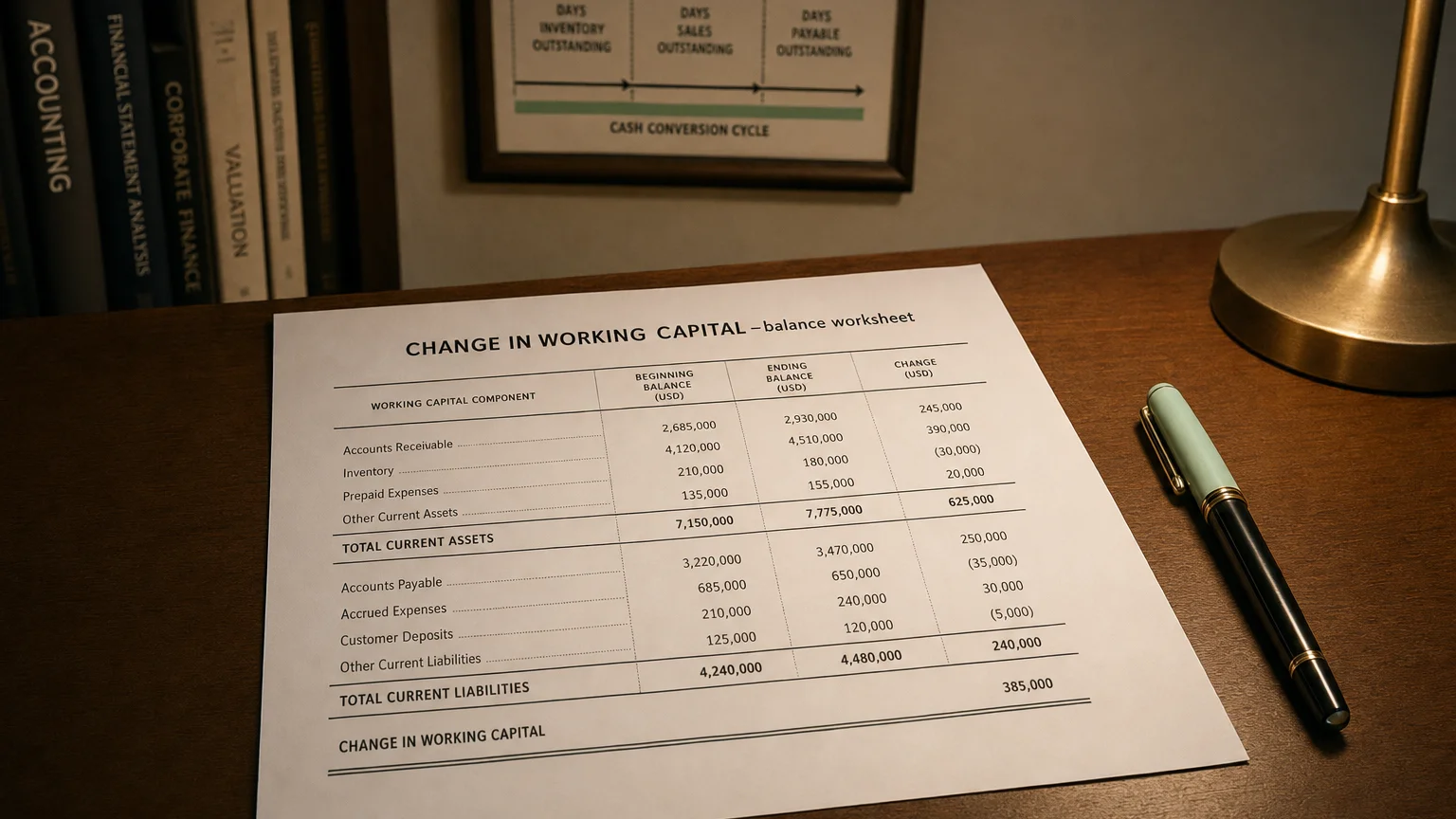

On the cash flow statement, the change in working capital is not usually a single line item. Instead, it’s presented as a series of adjustments within the Operating Activities section. The calculation begins with Net Working Capital (NWC):

Formula:

The change is then calculated by comparing the NWC of two periods. However, on the cash flow statement, you’ll see the individual changes:

The Rule of Thumb

Increases in operating assets (like inventory and receivables) are a use of cash and are subtracted. Increases in operating liabilities (like payables) are a source of cash and are added.

Component-by-Component Breakdown

- Accounts Receivable (AR): An increase in AR means more sales were made on credit than cash collected. This is a use of cash and is subtracted from net income.

- Inventory: An increase in inventory means the company spent cash to purchase goods that haven’t been sold yet. This is a use of cash and is subtracted.

- Accounts Payable (AP): An increase in AP means the company has delayed paying its own bills, effectively conserving cash. This is a source of cash and is added back.

- Other Current Liabilities: The same logic applies. An increase in an accrued expense (like unpaid wages) is a source of cash (added), while a decrease is a use of cash (subtracted).

Importance for Liquidity and Efficiency

Changes in working capital are a key indicator of a company’s liquidity and operational efficiency. Since working capital measures the short-term resources available for operations, its change shows how well a company can meet its immediate obligations. A company that consistently needs more cash to fund growing AR or inventory may have strained liquidity.

Working capital also reflects how efficiently a firm manages its operations. High working capital requirements could mean it’s slow to collect from customers or is holding onto too much unsold stock. As Investopedia explains, working capital “provides insight into the operational efficiency and overall financial health” of a business. Analysts compare operating cash flow to net income to assess how much cash the core business truly generates after these changes.

Interpreting the Business Signals

Shifts in working capital can signal growing pains or operational improvements. A rapidly expanding company may see working capital increase (a negative impact on cash flow) simply because it’s buying more inventory and extending more credit to new customers to fuel growth. In this case, a temporary drop in operating cash flow is expected.

An Investment in Growth

As noted by Morningstar, in growing firms, “changes in working capital is a little like capital spending: it’s money the company is investing—in things like inventory—in order to grow.”

However, an unusually large increase can also signal trouble, like ballooning inventory that isn’t selling. Conversely, a decrease in working capital (a positive impact on cash flow) often means the company is freeing up cash by collecting receivables faster or negotiating better payment terms. Monitoring these patterns helps investors understand whether cash flow trends are due to normal growth or operational strain.

Q · 01How can a profitable company have negative working capital changes?+

Q · 02What does a positive change in working capital signal on the cash flow statement?+