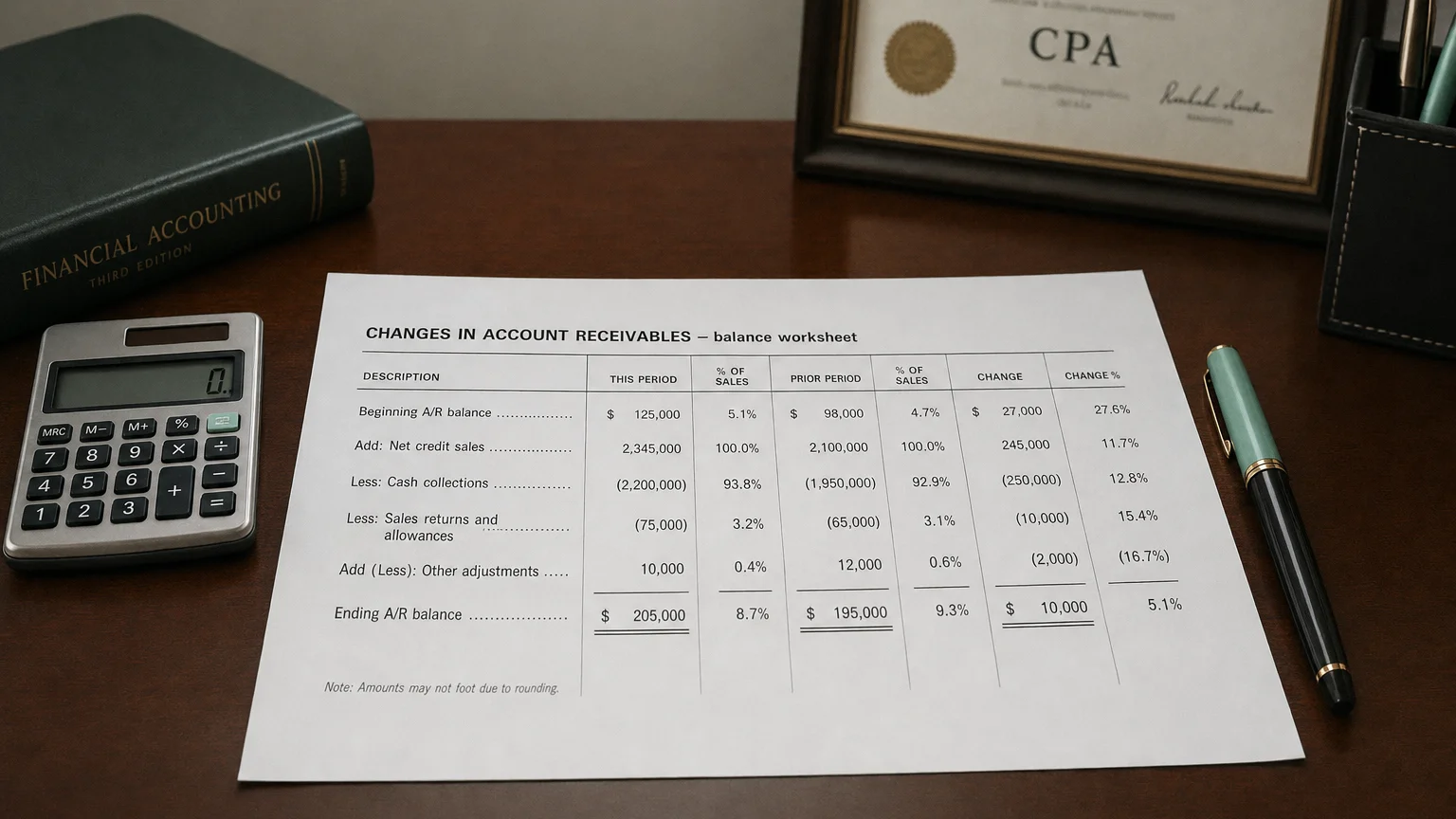

Changes in accounts receivable measures the period-over-period shift in customer credit balances. An increase reduces operating cash flow because revenue was recognized but not yet collected; a decrease adds cash because prior-period sales have been collected.

Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.

Changes in Accounts Receivable refers to the period-over-period difference in a company’s accounts receivable balance—the amount customers owe on credit sales. In simple terms, it measures how much the accounts receivable (AR) has increased or decreased compared to the previous period. This line item on the cash flow statement is a critical adjustment that shows how the change in customer IOUs impacts the company’s actual cash position.

Why Changes in Accounts Receivable Affect Cash Flow

“Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 2014 (2014)

This adjustment is necessary because of the fundamental difference between accrual accounting and cash reality. When a company sells on credit, it records revenue and profit immediately, even though no cash has been received. If accounts receivable increases, it means the company’s reported net income includes sales that have not yet been collected in cash. To get a true picture of cash flow, this non-cash portion of revenue must be removed. Therefore, an increase in receivables is subtracted from net income. Conversely, a decrease in receivables means the company collected cash from past sales, so this cash inflow is added back.

Increase vs. Decrease: A Source or Use of Cash?

The Core Rule

How It’s Calculated and Presented

The change is calculated as the difference between the ending and beginning receivables balances for the period. It appears in the Operating Activities section of the cash flow statement (indirect method).

Formula:

On the statement, an increase is typically shown in parentheses to indicate a subtraction from cash flow. For example, if receivables rise by 5,000)’.

Significance for Business Analysis

This line item is a powerful indicator of a company’s cash collection efficiency, working capital management, and quality of earnings. A large increase in receivables can be a warning sign that a company is having trouble collecting cash from its customers, potentially due to loose credit policies or a struggling customer base. This can strain liquidity, as profits on paper are meaningless if the cash isn’t coming in.

Conversely, a decrease in receivables is generally a positive sign, indicating that the company is effectively converting its sales into cash. Analysts often look at this trend in relation to sales growth. If receivables are growing faster than sales, it suggests that the quality of earnings may be deteriorating. Efficient companies strive to minimize the cash tied up in receivables, ensuring that profits are backed by strong, tangible cash flow.

Real-World Examples

Example: Apple Inc. (Fiscal 2022)

In its 2022 fiscal year, Apple’s cash flow statement showed an adjustment for ‘Accounts receivable, net’ of **(1.8 billion, which reduced its operating cash flow by that same amount. The company’s profits were higher than the cash it actually collected.

Example: ‘Dan’s Baseball Dugout’

In a hypothetical tutorial, a small business showed a ‘Decrease in accounts receivable: 1,000 from customers who owed money from previous periods, thereby increasing its operating cash flow.

Q · 01Why does an increase in accounts receivable reduce cash flow?+

Q · 02Where does this line item appear on financial statements?+