A key measure of the cash generated by a company's normal, day-to-day business operations, providing a vital look into its true profitability and liquidity.

When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.

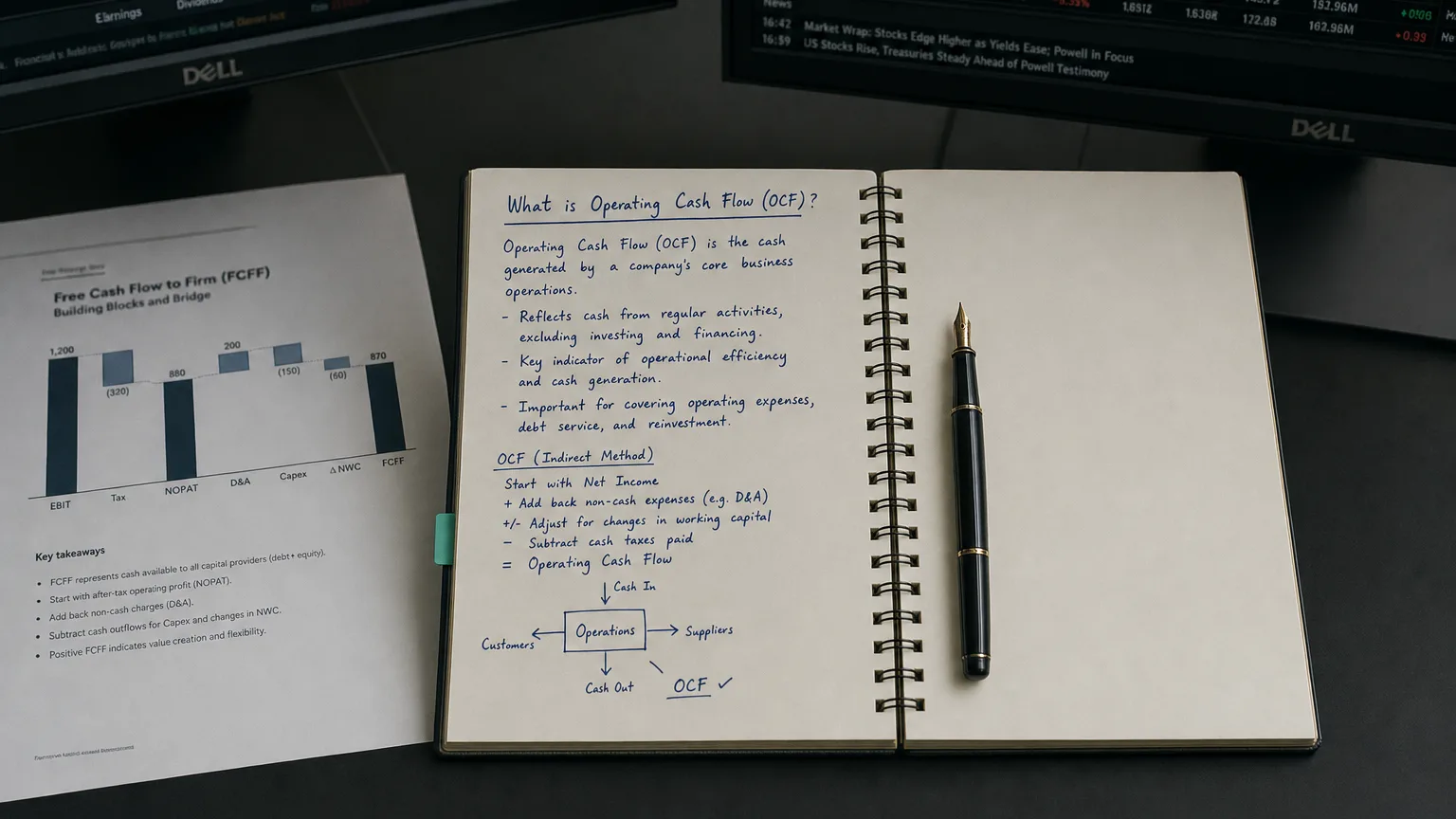

Operating Cash Flow (OCF) – also known as cash flow from operating activities – refers to the net amount of cash a company generates through its core business operations over a period of time. In essence, it measures cash inflows from selling products or services and cash outflows for operating expenses within that period. Operating cash flow excludes any cash movements related to investing (e.g. buying equipment) or financing (e.g. borrowing money or paying dividends) – it focuses solely on day-to-day business activities. A company’s OCF can be positive or negative: a positive OCF means the firm’s operating activities brought in more cash than they consumed (a net cash inflow), whereas a negative OCF means the operating activities used more cash than they generated (a net cash outflow) during that time.

Placement on the Cash Flow Statement

On the statement of cash flows, operating cash flow is typically the first section reported, preceding the investing and financing sections. This section is often titled “Cash Flows from Operating Activities.” Companies list the cash generated from operations at the top, then list cash flows from investing activities, and finally financing activities. At the end of the operating section, the total is shown as “Net cash provided by (used in) operating activities,” which represents the overall cash flow from operations for the period. (If this number is positive, it will be labeled “net cash provided by operating activities,” and if negative, “net cash used in operating activities” in real statements.)

Components of Operating Cash Flow

Operating cash flow encompasses all cash receipts and payments related to a company’s core operations. In practice, it consists of both cash inflows and outflows tied to running the business:

-

Cash inflows from operations include cash collected from customers for sales of goods or services. This can be direct cash sales or collections of credit sales (accounts receivable) and other operating cash receipts (like refunds or royalties received).

-

Cash outflows from operations include payments for the costs of running the business. Examples are cash paid to suppliers for inventory or raw materials, salaries and wages paid to employees, rent and utility bills, insurance, tax payments, and other operating expenses.

Changes in working capital (current assets and liabilities) are also a key component of OCF, since they affect the timing of cash flows. For instance, if customers pay off their outstanding invoices (a decrease in accounts receivable), that increases operating cash flow because more cash comes in. If the company buys more inventory (an increase in inventory on hand), that decreases operating cash flow because cash was spent to purchase those goods. Likewise, if the company delays paying its suppliers (an increase in accounts payable), it temporarily boosts cash flow because cash is retained longer. On the other hand, paying off expenses faster (like reducing accrued expenses) will reduce operating cash flow. All of these operational cash movements – cash receipts, payments, and the effects of working capital changes – combine to determine the net operating cash flow.

Calculating Operating Cash Flow (Indirect Method)

Most companies calculate operating cash flow using the indirect method, which starts with net income (from the income statement) and then adjusts it to convert accrual-based profit into actual cash flow. The basic formula under the indirect method can be summarized as:

Operating Cash Flow = Net Income + Non-Cash Expenses +/– Changes in Working Capital.

Using this approach, the computation involves a few steps:

-

Begin with net income: Start with the period’s net profit as reported on the income statement (this profit is accrual-based, not actual cash).

-

Add back non-cash expenses: Include expenses that reduced net income but did not use any cash. The most common non-cash expense is depreciation (and amortization), which allocates the cost of long-lived assets to expense but doesn’t actually consume cash in the period. Other non-cash items include amortization, stock-based compensation, impairment charges, deferred taxes, or unrealized gains/losses – these are all added back because no cash was paid out for them.

-

Adjust for changes in working capital: Add or subtract the net change in current assets and current liabilities related to operations. For example, increase in accounts receivable is subtracted (it represents revenue earned that hasn’t been received in cash, reducing cash flow), increase in inventory is also subtracted (cash was spent to buy inventory). In contrast, an increase in accounts payable is added (the company held onto its cash by delaying payment), and an increase in other accrued liabilities would also be added. Decreases in these accounts would have the opposite effects (e.g. a drop in receivables means more cash collected, so it increases OCF).

-

Remove any non-operating gains or losses: If net income includes items from investing or financing activities (such as a gain from selling equipment), those are backed out of operating cash flow because they are not part of core operations. This ensures OCF reflects only operating activities.

After these adjustments, the result is the net cash provided (or used) by operating activities for the period.

Example calculation: Suppose a company has a net income of $50,000 for the year. It records a depreciation expense of $10,000 (non-cash), accounts receivable increased by $5,000, inventory increased by $3,000, and accounts payable increased by $8,000. Using the indirect method: start with $50,000 net income, add back $10,000 depreciation, subtract the $5,000 increase in receivables, subtract the $3,000 increase in inventory, and add the $8,000 increase in payables. The resulting operating cash flow would be $60,000 ($50k + $10k – $5k – $3k + $8k). This $60,000 represents the actual cash generated from the company’s operations, which can differ from the net income due to those working capital timing differences and non-cash charges.

(Note: Companies can also report OCF using the direct method, which skips the net income reconciliation and instead directly lists cash received from customers and cash paid for expenses. However, the indirect method described above is more commonly used in practice and both methods should arrive at the same OCF figure in the end.)

Importance for Financial Health

Operating cash flow is considered a vital indicator of a company’s financial health and sustainability. Unlike net income (which can be influenced by non-cash accounting entries or timing of revenue and expenses), OCF shows the actual liquidity generated by the business’s core operations. Analysts and investors look at OCF to assess whether a company’s normal business activities are generating enough cash to pay its bills, fund new projects, and service debts. In fact, many view the operating cash flow section as the most informative part of the cash flow statement for judging a firm’s performance and viability.

A strong OCF means the company is efficiently converting its revenues into real cash. For example, if one company has high sales but most of those sales are on credit (accounts receivable), it might show high profit but low OCF – indicating cash isn’t coming in quickly. Another company with more modest sales largely in cash could actually have a higher OCF, meaning it has more readily available cash from its operations. Thus, OCF gives insight into operational efficiency (how well the firm turns sales into cash) and liquidity (ability to meet short-term obligations).

Crucially, operating cash flow also signals whether a company can self-fund its activities. Consistently positive OCF provides a business with internal funds to reinvest in equipment, expand inventory, or develop new products without needing to raise external capital. It also improves a company’s ability to pay down debt and handle unexpected expenses, since cash is available from the business itself. In contrast, a company with weak or negative operating cash flow might struggle to sustain operations or grow without borrowing money or issuing stock.

Strong vs. Weak Operating Cash Flow

Strong operating cash flow – generally characterized by steady, positive OCF – is a sign of financial strength. Companies with strong OCF are typically in a better position financially than those with weak or negative OCF. Robust operating cash flow means the firm’s core business is generating ample cash, which can cover operating costs, fund new investments, and potentially be returned to shareholders (through dividends or buybacks) after meeting obligations. Investors and creditors often prefer to see healthy OCF because it suggests the company can finance itself and is less likely to default on obligations. For instance, a consistently positive (and growing) OCF indicates the business can pay its bills and reinvest in growth without relying on external financing or selling assets. It’s not uncommon for analysts to calculate the operating cash flow ratio (OCF divided by current liabilities) as a quick test of liquidity – a ratio above 1.0 is generally good, indicating current debts can be paid by operating cash flow alone.

On the other hand, weak or negative operating cash flow can be a warning sign. If a company’s OCF is persistently negative or far lower than its net income, it means the company isn’t actually collecting enough cash from its operations to cover its outflows. Ongoing negative operating cash flow could indicate financial trouble or liquidity issues. Such a company might be forced to dip into savings, sell investments, or seek external financing (like bank loans or new equity) just to keep operating. For example, a firm might report accounting profits but have trouble paying suppliers or creditors on time if most of its sales haven’t yet turned into cash – this situation would reflect in a weak OCF. In extreme cases, consistently negative OCF can threaten a company’s solvency if it cannot raise cash elsewhere.

It’s worth noting there are scenarios (such as early-stage startups or high-growth companies) where operating cash flow might be temporarily negative due to aggressive growth spending or extended credit to customers. Many startups have negative operating cash flow in their first years because they are investing heavily in the business (increasing expenses and inventory) faster than their sales are growing. In such cases, negative OCF isn’t necessarily “failure,” but it does underscore the reliance on external funds until the business model matures. Ultimately, however, a company must eventually turn its operating cash flow positive to be financially self-sustaining in the long run.

Example in a Real-World Cash Flow Statement

To see how operating cash flow appears on an actual financial statement, consider a large company’s annual report. The cash flow statement is divided into three sections, with Operating Activities listed first, followed by Investing and Financing. Within the operating section, the statement typically begins with “Net income” (from the income statement), then adds or subtracts various adjustments to reconcile net income to cash flow. These adjustments are the non-cash expenses and working capital changes discussed above (for example: “Depreciation expense – added back,” “Increase in accounts receivable – subtracted,” etc.). After listing all the adjustments, the section ends with a line labeled “Net cash provided by (used in) operating activities”, which is the final tally of operating cash flow for that period.

For instance, Amazon.com Inc. reported “Net cash provided by operating activities” of $115.9 billion for the year 2024. This means Amazon’s core businesses (e.g. its online stores, AWS cloud services, etc.) collectively generated a positive cash inflow of nearly $116 billion in that year. In Amazon’s cash flow statement, you would see net income as a starting point, then large add-backs for non-cash costs like depreciation and amortization, and adjustments for changes in receivables, inventories, payables, and other operational items – all summing up to that $115.9 billion OCF. By contrast, its investing and financing sections for 2024 showed net cash outflows (as Amazon spent cash on investments and paid down financing). This example illustrates how a healthy, mature company can produce substantial operating cash flow, which it can then use to fund investments (like new facilities or equipment) or return to investors, while still maintaining a strong cash position.

In summary, Operating Cash Flow is a key figure for anyone analyzing a company’s finances. It reveals the cash-generating power of the core business and is crucial for evaluating profitability in cash terms, liquidity, and overall financial stability. Strong operating cash flow generally indicates a company is financially sound and internally sustainable, whereas weak operating cash flow can highlight potential issues that may not be obvious from net income alone. Understanding OCF helps investors, creditors, and managers determine whether a company’s profits are real and repeatable in cash terms – or if additional scrutiny (and possibly corrective action) is needed to improve the company’s cash flow health.