Other Intangible Assets is a financial concept covered in this article. Separately Identifiable Acquired Intangibles Excluding Goodwill

When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.

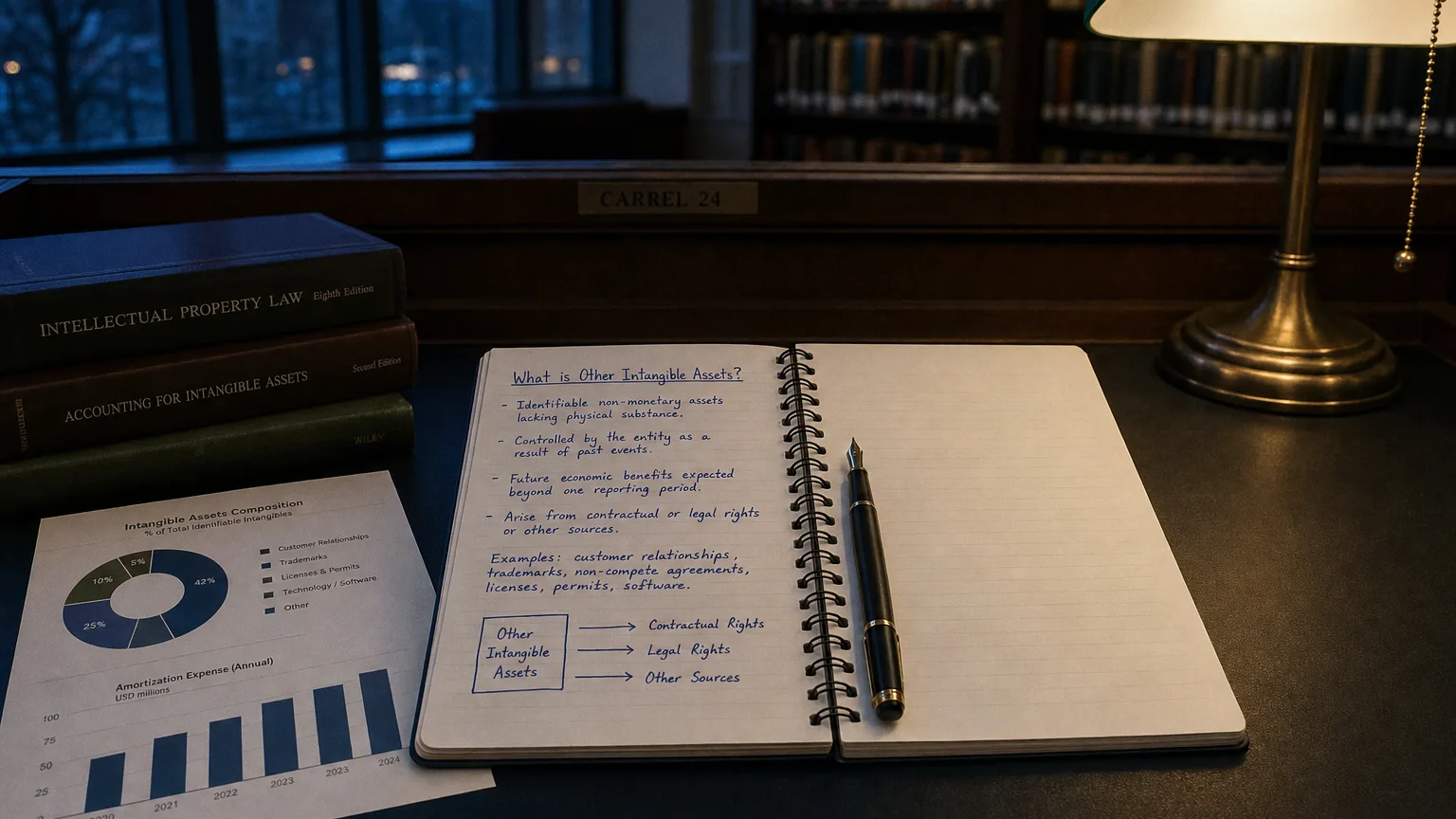

Other Intangible Assets encompass all acquired intangible assets that are separately identifiable and measurable apart from goodwill. These non-physical assets provide future economic benefits through contractual rights, legal protections, or separability, and are recognized in business combinations or separate purchases. They are presented net of accumulated amortization (for finite-life assets) or impairment.

Definition and Recognition Criteria

Other Intangible Assets are recognized if they are:

- Separately identifiable (capable of being separated/sold or arising from contractual/legal rights)

- Controlled by the entity

- Expected to provide future economic benefits

Unlike goodwill (residual premium), these assets are valued independently in acquisitions.

Internally developed intangibles are expensed as incurred (R&D, advertising) except specific software development costs.

“When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1985 (1985)

Common Types

Finite-Life Intangibles

- Customer relationships/contracts/lists

- Technology/patents/developed software

- Order backlog

- Non-compete agreements

- Licenses/franchises with fixed terms

- Favorable contracts

Indefinite-Life Intangibles

- Trademarks/trade names with indefinite renewal

- Certain internet domain names

- Broadcast licenses (if perpetually renewable)

Useful lives typically 3–20 years for finite assets.

Accounting Treatment

Key rules:

Finite-Life

- Amortized over estimated useful life (straight-line common)

- Residual value usually zero

- Method reflects pattern of economic benefit consumption

- Impairment tested if indicators present

Indefinite-Life

- No amortization

- Annual impairment test + trigger-based

Impairment losses recognized immediately; reversals prohibited for most under US GAAP.

Balance Sheet Presentation

Under non-current assets as:

- ‘Other Intangible Assets’

- ‘Intangible Assets, net’

- Gross cost less accumulated amortization/impairment

- Often combined with goodwill but disclosed separately

Footnotes provide rollforward, major classes, remaining lives, amortization expense.

Valuation in Acquisitions

In business combinations:

- Fair value at acquisition date

- Common methods: Relief-from-royalty (trademarks), Multi-period excess earnings (customer relationships), With/without (non-compete)

Higher allocation to identifiable intangibles reduces goodwill.

Analytical Implications

These assets impact analysis by:

- Amortization expense reduces ongoing earnings

- Impairment signals overvaluation or lost value

- Indicate competitive advantages (brands, technology)

- Sector-specific importance (high in tech, media, pharma)

- Tangible vs. total assets comparison

Heavy amortization burden can mask underlying cash earnings.