Other Receivables (Non-Trade Receivables) is a financial concept covered in this article.

In the short run, the market is a voting machine. In the long run, it is a weighing machine.

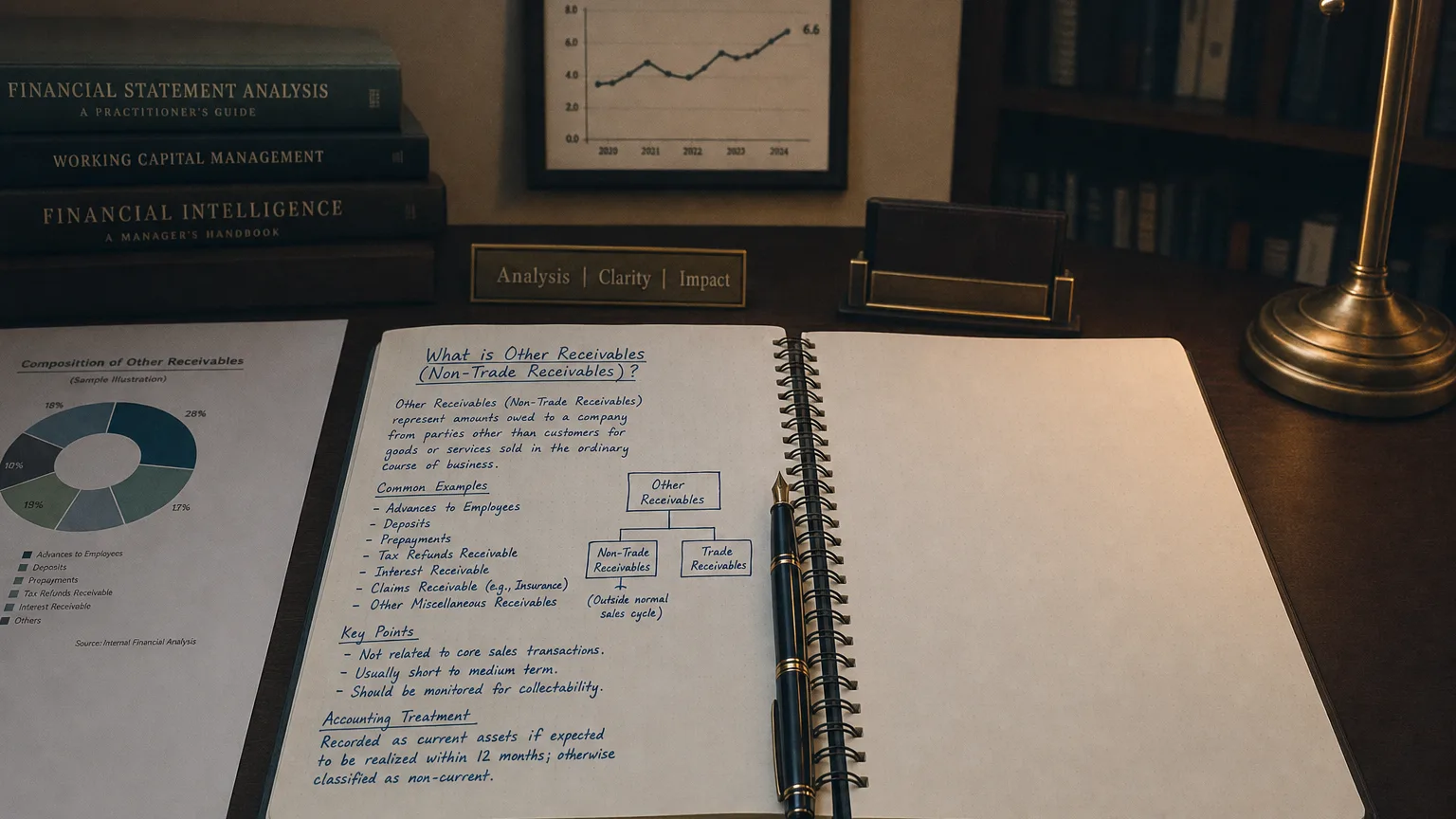

Other receivables (also called non-trade receivables) are amounts owed to a company that do not arise from its normal sales to customers. In other words, they are claims a company expects to collect that are outside of its core business transactions. For example, if a company has earned interest on a loan or is due a tax refund from the government, these amounts would be booked as other receivables. They are reported as assets on the balance sheet, separate from the primary ‘Accounts Receivable’ line.

Trade Receivables vs. Other Receivables

The fundamental difference lies in the source of the transaction. Trade receivables, commonly known as Accounts Receivable (AR), arise exclusively from a company’s routine sales of goods or services on credit to its customers. In contrast, Other Receivables are claims generated from non-sales activities.

At a Glance

- Accounts Receivable: Money owed by customers from sales.

- Other Receivables: Money owed by other parties for non-sales reasons.

“In the short run, the market is a voting machine. In the long run, it is a weighing machine.”

— Benjamin Graham, Author, The Intelligent Investor Security Analysis (1934)

Common Examples of Other Receivables

The ‘Other Receivables’ category can include a diverse set of items. Typical examples include:

- Interest Receivable: Interest earned on investments like bonds or loans that has not yet been received in cash.

- Income Tax Receivable: Tax refunds owed to the company by the government due to overpayment or tax credits.

- Advances to Employees: Short-term loans or salary advances given to staff that are expected to be repaid.

- Dividends Receivable: Dividends that have been declared by a company in which you own shares but have not yet been paid out.

- Insurance Claims Receivable: Amounts due from an insurance company for a filed claim.

Presentation and Importance in Financial Analysis

On the balance sheet, Other Receivables typically appear under Current Assets if they are expected to be collected within one year. Companies may list them on a separate line or group them with trade receivables under a heading like “Accounts and Other Receivables.”

Why Analysts Separate Them

Understanding the amount of other receivables is crucial for accurate financial analysis. Performance metrics that measure collection efficiency, like Days Sales Outstanding (DSO) or the accounts receivable turnover ratio, should ideally be calculated using only trade receivables. Including non-trade items like a large, one-time tax refund would distort these ratios and give a misleading impression of how quickly the company collects from its customers. Separating them allows for a clearer view of a company’s core operational performance.